- We always suggest you use a CPA that understands the special status of ministers and the employee reimbursement system (EOM system). This is called by the IRS an accountable reimbursement plan.

- Missionaries are NOT non-profit organizations in and of themselves UNLESS they create their own non-profit. This means you cannot give a charitable donation receipt to an individual for an offering they give to you directly. For individuals to claim a charitable donation, they must give through FBMI to you.

- NOTE: Some missionaries set up on their web sites the ability for people to donate directly to their ministries through methods such as credit cards, paypal, gofundme, etc. ALL monies received in this manner should be entered on the EOM in BOX C so you will be able to claim them as work fund expenses when used as such.

Here is how tax withholding works based upon your employment status.

1. Employee in any job here in the US.

a. Federal tax: Employer withholds %100 tax due.

b. Social Security & Medicare: Employer withholds from your paycheck %50 tax due.

Employer Pays for the remaining %50 tax due.

2. Self Employed Individual (own your own business)

a. Federal tax: self-employed person pays %100 tax due.

b. Social Security & Medicare: self-employed person pays %100 tax due.

3. Deputation missionary is treated like a regular employee (mentioned in #1 above).

a. Federal tax: FBMI withholds from your voucher %100 tax due.

b. Social Security & Medicare: FBMI withholds from your voucher %50 tax due.

FBMI Pays for the remaining %50 tax due.

c. No Housing allowance is allowed until you get to the field.

NOTE: Those based in the US as evangelists and have a base home will be allowed a housing allowance once ordained and fully commissioned.

4. Missionary on the field

a. Federal tax: FBMI withholds from your voucher %100 tax due.

NOTE: Housing allowance for ordained and commissioned missionary allowed BUT NO federal tax is due on this housing amount.

b. Social Security & Medicare: Missionary is responsible for %100 of this tax. FBMI DOES NOT withhold this tax.

- This tax is due on all salary received. FBMI DOES NOT withhold this tax.

2.This tax is due on ALL housing allowance amounts. FBMI DOES NOT withhold this tax.

3.This is a tax of over %15.

4. You will be responsible for paying this tax by using form SE when filing your taxes.

5. Since you have never had to pay this tax in this manner previously, it would be wise for you to have some tax withheld each month on your first year “on the field”. This will help you not to have a “surprise” at the end of that first year when you file your taxes.

- In order to receive Social Security and Medicare benefits when you get to retirement age, you MUST pay into the system by using FORM SE when filing your taxes each year.

- The services you perform in the exercise of your ministry are generally covered by social security and Medicare under the self-employment tax system. This means that your salary on Form W-2, Wage and Tax Statement, the net profit on Schedule C, and your housing allowance less pertinent deductible expenses are subject to self-employment tax on Schedule SE (Form 1040), Self-Employment Tax. Your earnings for these ministerial services are subject to self-employment (SE) tax unless one of the following applies.

- You are a member of a religious order who has taken a vow of poverty.

- You ask the IRS for an exemption from SE tax for your services and the IRS approves your request. See Exemption From Self-Employment (SE) Tax , later.

- You are subject only to the social security laws of a foreign country under the provisions of a social security agreement between the United States and that country. For more information, see Bilateral Social Security (Totalization) Agreements in Pub. 54.

The tax rate for the social security part is 12.4%. In addition, all of your net earnings are subject to the Medicare (hospital insurance) part of the SE tax. This tax rate is 2.9%. The combined self-employment tax rate is 15.3%. For services in the exercise of the ministry, members of the clergy receive a Form W-2, but do not have social security or Medicare taxes withheld. You must pay social security and Medicare taxes by filing Schedule SE (Form 1040) with your return.

- The fair rental value of the housing allowance is excludable only for income tax purposes. The minister must include the amount of the fair rental value of a parsonage or the housing allowance for social security coverage purposes. This exclusion applies only for income tax purposes. It doesn’t apply for SE tax purposes. Why do we have you fill out a housing allowance each year? Because of the IRS requirement noted here.

The church or organization that employs you must officially designate the payment as a housing allowance before it makes the payment. It must designate a definite amount. It can’t determine the amount of the housing allowance at a later date. If the church or organization doesn’t officially designate a definite amount as a housing allowance, you must include your total salary in your income.

- You can request an exemption from self-employment tax for your ministerial earnings, if you’re opposed to certain public insurance for religious or conscientious reasons. You can’t request exemption for economic reasons. But this MUST be done within 2 years of when you start receiving income as a minister. To request the exemption, file 4361 with the IRS.

- I believe everyone should stay in the Social Security System. Why?

- The exemption is for those with a religious conviction or conscientious conviction, not just economic reasons.

- Some who got out of the SS system, did not practice the economic strategy of putting the money not going into SS into a retirement fund. This often results in the minister and/or his wife not having anything to fall back on in their old age, when they had physical problems (disability) or when the husband dies.

- Most likely the only way we will not have a SS system in this country is when the whole economic system fails. In other words, the politicians will keep funding it.

- Preparation for retirement. There are many options for someone to prepare for retirement. I will mention just two avenues here.

- Roth IRA. With a Roth IRA, you do not pay taxes on any interest or dividends earned through the life of the IRA.

- Traditional IRA which can be a 403(b) plan. You only pay tax on this when you withdraw the money from the account.

Income Tax Withholding and Estimated Tax

The federal income tax is a pay-as-you-go tax. You must pay the tax as you earn or receive income during the year. An employee usually has income tax withheld from his or her wages or salary. However, your salary isn’t subject to federal income tax withholding if both of the following conditions apply.

- You are a duly ordained, commissioned, or licensed minister, a member of a religious order (who hasn’t taken a vow of poverty), or a Christian Science practitioner or reader.

- Your salary is for ministerial services (see Ministerial Services , earlier).

If your salary isn’t subject to withholding, or if you don’t pay enough tax through withholding, you may need to make estimated tax payments to avoid penalties for not paying enough tax as you earn your income.

You must generally make estimated tax payments if you expect to owe taxes, including SE tax, of $1,000 or more, when you file your return.

Self-employment tax.

For services in the exercise of the ministry, members of the clergy receive a Form W-2, but do not have social security or Medicare taxes withheld. You must pay social security and Medicare taxes by filing Schedule SE (Form 1040) with your return.

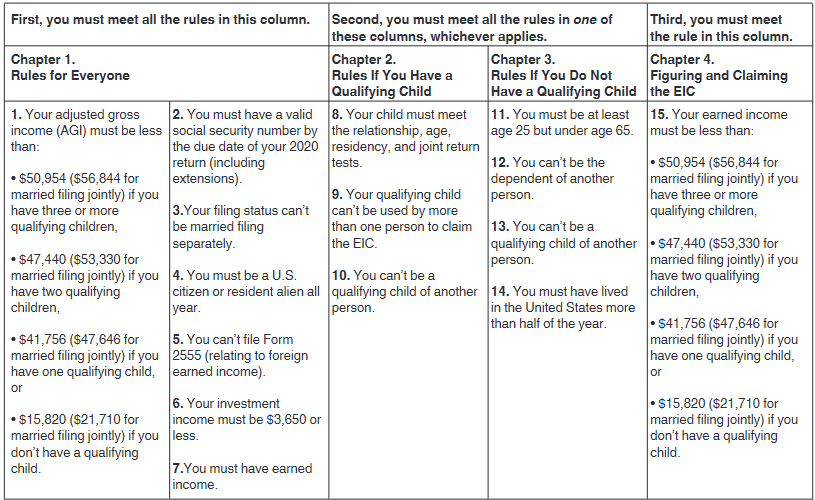

Earned Income Tax Credit